Bunker prices skyrocket in Week 11 on Middle East Crisis

Global bunker fuel prices surged by approximately 30–35% over the past week, driven by escalating tensions between the United States and Iran and the effective closure of the Strait of Hormuz, a critical global oil transit chokepoint. The disruption triggered a sharp rally in crude oil markets, pushing major benchmarks to multi-year highs and significantly increasing volatility across the global energy complex.

According to Sergey Ivanov, Director, MABUX, “The current geopolitical escalation is creating unprecedented pressure on bunker markets, triggering rapid price increases across all fuel segments.”

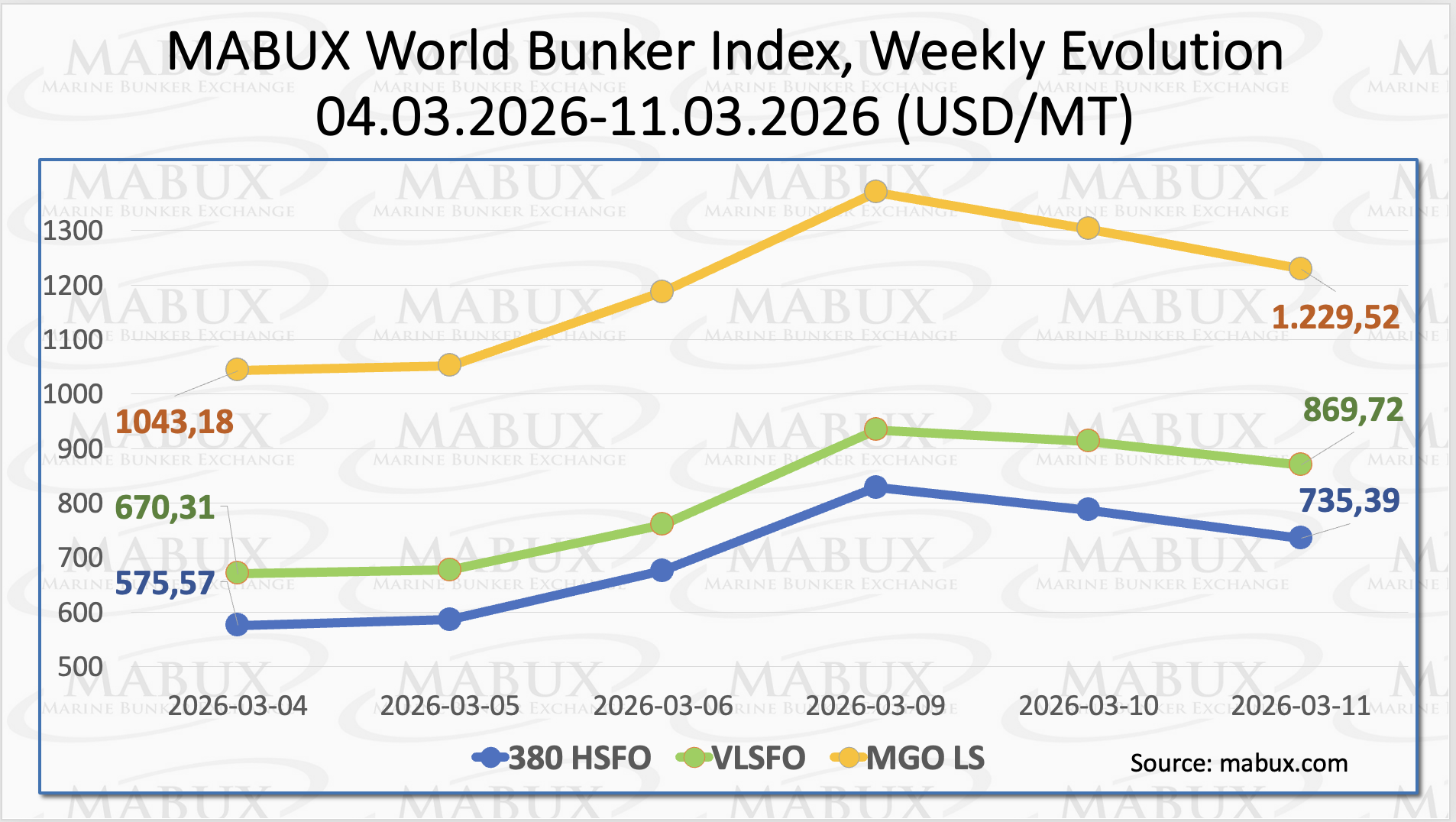

The MABUX Global 380 HSFO Index rose by US$ 159.82, increasing from US$ 575.57/MT last week to US$ 735.39/MT. The VLSFO Index posted an even stronger advance, climbing by US$ 199.41, from US$ 670.31/MT to US$ 869.72/MT. The MGO LS Index also recorded a sharp increase, rising by US$ 186.34, from US$ 1,043.18/MT last week to US$ 1,229.52/MT, briefly exceeding the US$ 1,300.00/MT mark—the highest value recorded since MABUX data tracking began in 2001. Ivanov commented that “Such extreme volatility is likely to continue as long as regional tensions remain unresolved and oil supply routes are restricted.”

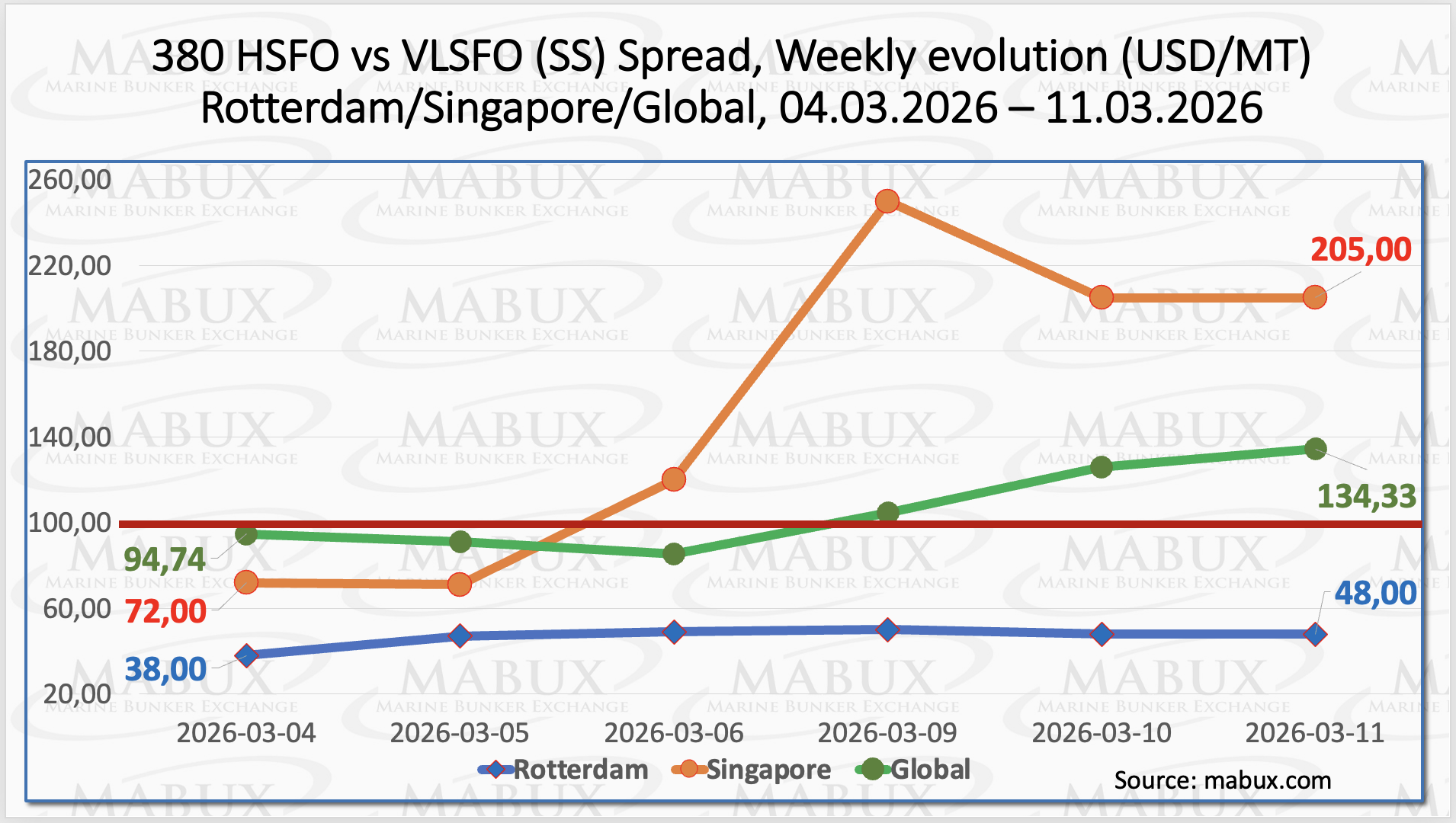

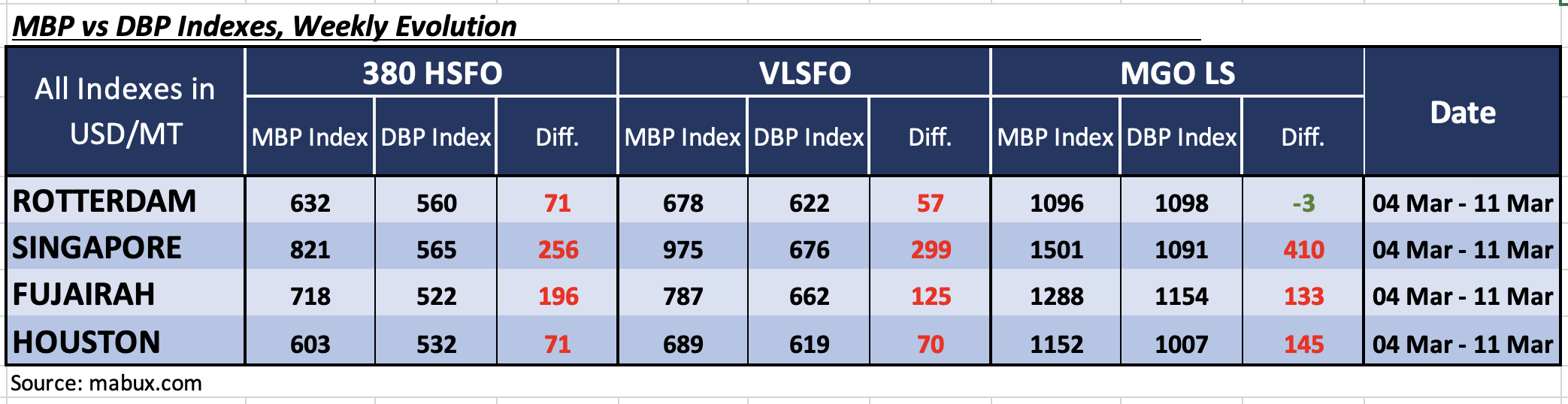

The MABUX Global Scrubber Spread (SS)—the price differential between 380 HSFO and VLSFO—increased sharply, rising by US$ 39.59, from US$ 94.74 last week to US$ 134.33, significantly exceeding the US$ 100.00 breakeven threshold for scrubber economics. In Rotterdam, the SS Spread rose by US$ 10.00, reaching US$ 48.00, while the weekly average in the port decreased by US$ 2.66. Singapore recorded the most pronounced surge, with the 380 HSFO/VLSFO differential climbing US$ 133.00, from US$ 72.00 to US$ 205.00, at one point briefly reaching US$ 250.00. The weekly average SS Spread in Singapore increased by US$ 73.33.

Sergey Ivanov added: “The widening of the SS Spread in Singapore highlights acute regional fuel shortages and ongoing supply disruptions.”

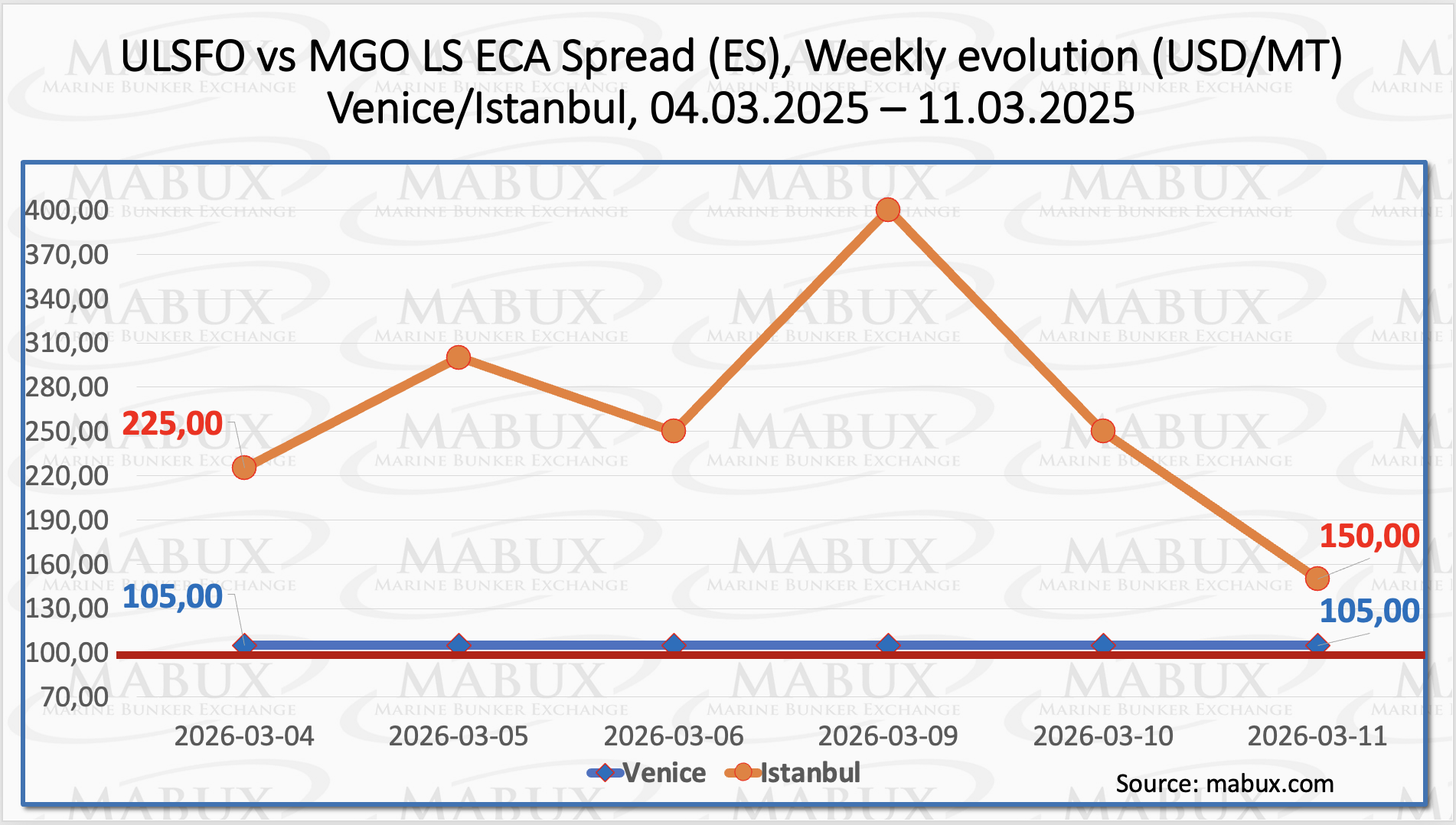

At the end of the week, the ECA Spread (ES) in Istanbul declined by US$ 75.00, from US$ 225.00 to US$ 150.00, though it temporarily surged to around US$ 400.00 during the week. The weekly average advanced by US$ 123.33, reflecting extreme fluctuations in distillate prices. In Venice, the ES remained at US$ 105.00, although limited fuel availability reduces the reliability of quotations. Ivanov said: “ECA spreads are extremely sensitive to regional diesel price swings under current geopolitical conditions.”

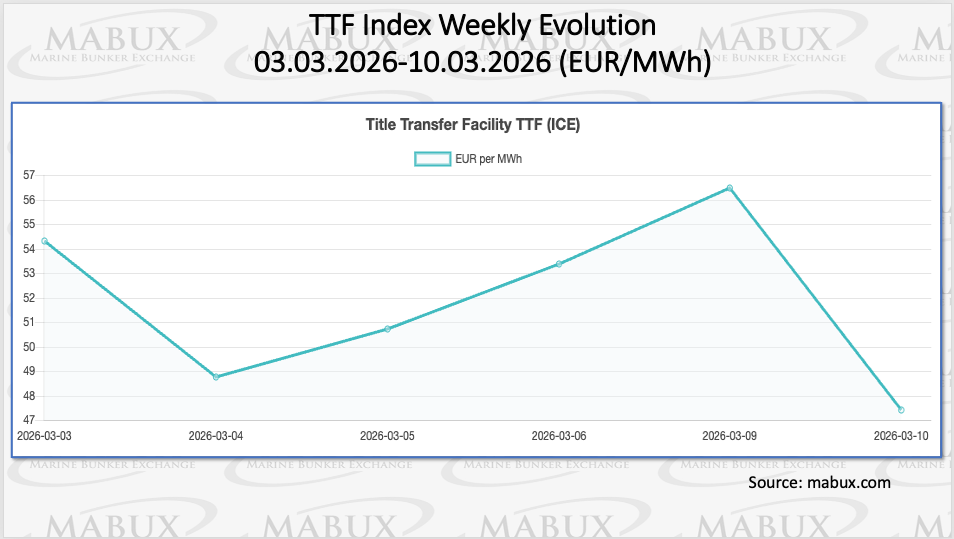

Military escalation in the Middle East and the effective closure of the Strait of Hormuz triggered a sharp reaction in European gas markets. The Title Transfer Facility (TTF) benchmark rose significantly amid concerns over potential disruptions to global LNG flows. As of 10 March, European underground gas storage levels continued to decline, reaching 29.29% of total capacity, down 0.60 percentage points from the previous week and 32.17 points below 1 January 2026 levels (61.46%). The TTF benchmark declined moderately by €6.897/MWh, from €54.290/MWh to €47.393/MWh, remaining near the €50/MWh level.

LNG bunker prices at the port of Sines (Portugal) surged by US$ 764.00, reaching US$ 1,538/MT, compared with US$ 774/MT the previous week. The price differential between LNG and conventional marine fuel shifted in favor of conventional fuel, reaching US$ 188 in favor of MGO LS. On March 9, MGO LS at Sines was quoted at US$ 1,350/MT. Ivanov commented: “The combination of LNG supply disruptions and geopolitical tension is creating unprecedented regional price swings.”

Amid heightened volatility, the MABUX Market Differential Index (MDI) shifted into the overvaluation zone across all major bunkering hubs: Rotterdam, Singapore, Fujairah, and Houston:

-

380 HSFO segment: Overvaluation surged by 66 points in Rotterdam, 230 points in Singapore, 159 points in Fujairah, and 83 points in Houston. Singapore and Fujairah MDIs moved well above US$ 100.00, indicating a major divergence from the MABUX digital benchmark.

-

VLSFO segment: Overvaluation increased by 55 points in Rotterdam, 289 points in Singapore, 125 points in Fujairah, and 42 points in Houston. Singapore and Fujairah MDIs significantly exceeded US$ 100.00, reflecting strong upward pressure on market prices.

According to Wood Mackenzie, amid the escalating conflict in the Middle East and the disruption of approximately 15 million barrels per day (bpd) of supply from the Persian Gulf, a reduction in global oil demand across several sectors may be required to rebalance the market. Under these conditions, crude oil prices could potentially rise to around USD 150 per barrel in the coming weeks. Such a scenario would act as a major upward driver for bunker fuel prices, further intensifying pressure on the global bunker market. Given the current geopolitical environment and tightening supply conditions, rising bunker fuel prices are likely to remain the dominant trend in the near term.

The post Bunker prices skyrocket in Week 11 on Middle East Crisis appeared first on Container News.

Content Original Link:

" target="_blank">

: Κέρδη 9,9 εκατ. δολάρια και ρευστότητα 353,3 εκατ. δολάρια")